WHAT THE NEW TAX LAW MEANS FOR YOU AS A CRYPTO HOLDER

Tuesday, October 28, 2025

If you’ve been trading, staking, or holding crypto in Nigeria, you’ve probably heard talks, seen videos, and tweets about the 2026 tax reforms. Those talks are now facts. The Nigerian government has made it clear: crypto is no longer outside the system.

From January 1, 2026, gains from your digital assets: Bitcoin, Ethereum, stablecoins, NFTs, and more, will officially fall under the new national tax framework.

Let’s break down what that means for you as a crypto holder.

1. The Law Is Changing, and It’s Coming for Digital Assets

The 2026 Finance Act broadens Nigeria’s tax base to include all income and gains, regardless of where or how they are earned. This means that if you are a Nigerian resident, any income you earn — including income from cryptocurrency — may be taxable.

Until now, the decentralized nature of crypto has made taxation unclear. But with this new law, the Federal Inland Revenue Service (FIRS) now has the mandate and the digital tools to include crypto profits as part of taxable income.

Whether you are a casual trader or a full-time investor, the taxman is now part of the blockchain conversation.

2. You’ll Only Be Taxed on Profits, Not on Your Wallet Balance

The government will not tax your crypto holdings. You only owe tax when you make a profit, that is, when you sell or swap your assets for more than you bought them.

For example:

If you buy ₦1,000,000 worth of Bitcoin and later sell it for ₦2,000,000, your taxable gain is ₦1,000,000. You are not taxed on the total ₦2,000,000.

If you are holding your crypto without selling, there is no realized gain yet, and therefore, no tax.

3. There’s a Threshold, but It’s Smaller Than You Think

Under the new law, individuals will not pay income tax on their first ₦800,000 of total annual earnings, which includes crypto profits.

So, if you earn ₦500,000 from your job and ₦200,000 trading crypto, you remain under the threshold. However, if your combined income, from salary, business, and crypto, exceeds ₦800,000 in a year, you become liable for income tax.

For larger investors, there is another layer of relief. If your total disposals in a year are less than ₦150 million and your total gains do not exceed ₦10 million, you may qualify for an exemption under the Capital Gains Tax (CGT) rules. This gives small traders and part-time investors some breathing room.

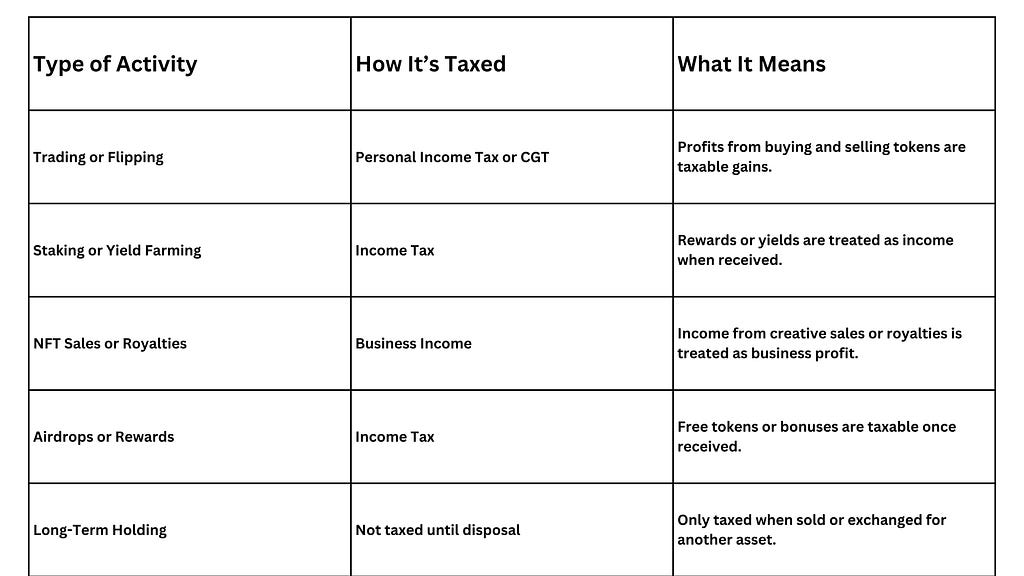

4. Different Kinds of Crypto Earnings, Different Tax Treatments

Not all crypto profits are treated the same. The law recognizes different categories of earnings:

Whether you’re flipping tokens, farming yields, or creating NFTs, your tax liability depends on what you’re doing, not just what you own.

The Real Challenge Isn’t the Tax, It’s the Records

To determine what you owe, you’ll need accurate documentation for every transaction. That includes:

- The date you bought the crypto

- The amount paid in Naira (your cost basis)

- The date and amount when you sold or converted

- Fees or commissions paid

How to Stay Ahead

Here are the steps every crypto holder should take before 2026:

- Keep detailed records of your trades and conversions

- Separate your long-term wallet from your trading wallet

- Use crypto tax software to calculate realized gains

- Consult a tax accountant familiar with digital assets

- Declare income voluntarily to build a compliance record

- Plan your cash-outs strategically to stay under taxable thresholds

If you use Divest to convert crypto to cash, make sure you save your conversion receipts and transaction summaries. They’ll help you verify your taxable position later.

Recent Posts

Nothing Humiliates an IJGB Faster Than a POS Decline in Detty December.

Read More »The Hidden Costs of Bulk Crypto-to-Cash Conversions, And How to Avoid Them

Read More »Why Waiting 3 Days to Cash Out Crypto Is Old School

Read More »Bulk Crypto Conversion Without the Hassle: A Guide for CFOs and Finance Teams

Read More »